Rent Affordability Rules UK often determine whether you can successfully rent a property. Imagine finding the perfect rented property. The location is ideal, the price looks sensible, and you can already picture yourself living there.

But when you send your application, the property owners reject it because you fail the affordability checks required under the Rent Affordability Rules UK.

This situation surprises thousands of renters across the UK every year.

Many people focus only on whether they can make the monthly rent payment. However, landlords and letting brokers look at much more than that. They want proof that tenants can comfortably afford the property without struggling financially.

Understanding the Rent Affordability Rules UK before starting your property search can save time, reduce stress, and improve your chances of approval.

This guide reflects standard UK letting industry practice as of 2026, including affordability benchmarks commonly cited by referencing agencies and organisations such as Shelter and the National Residential Landlords Association (NRLA). Individual landlord criteria vary, so always confirm specific requirements with the letting agent before applying.

Let’s explore how the Rent Affordability Rules UK work in the UK and how you can calculate a rental budget that suits your finances.

Read more:Rent vs Buy Calculator UK – Should You Rent or Buy a HomeWhat Are Rent Affordability Rules in the UK?

Rent affordability rules are guidelines used by property owners, letting agents, and referencing companies to Judge whether a renter can comfortably afford a rental property.

These checks are designed to reduce the risk of missed rent payments and ensure that tenants are not financially overloaded

In simple terms, affordability checks compare a tenant’s income with the cost of rent to see if the rental is practically manageable, together with other living expenses such as bills, food, transport, and Loan payments

A commonly used rule in the UK states that a tenant’s annual earnings should be at least 30 times the rent per month.

- Income Requirement: For example, if the rent is £800 per month, the tenant would typically need an annual income of at least £24,000.

- 30%–40% Income Rule: Another widely used benchmark is that rent should not exceed 30% to 40% of a tenant’s monthly income.

- 2.5–3 Times Rent Rule: Many letting agents also apply a “2.5 to 3 times monthly rent” rule, meaning your gross monthly income should be at least 2.5–3 times the rent amount.

- Affordability Assessment: In addition to income checks, landlords often carry out full affordability assessments, which may include reviewing bank statements, credit history, employment status, and existing financial commitments.

- Stress Test: Some agencies also apply a “stress test” to ensure tenants can still afford rent if their expenses increase or their income drops slightly.

Read more:Rent Affordability Rules UK – How Much Rent Can You Afford| Monthly Rent | Recommended Annual Income |

|---|---|

| £800 | £24,000 |

| £1,000 | £30,000 |

| £1,200 | £36,000 |

| £1,500 | £45,000 |

This method helps reduce the risk of missed payments and financial difficulties for both renters and landlords.

Why Do Rent Affordability Rules Matter?

| Benefit | Description |

|---|---|

| Prevent financial stress | Help renters avoid taking on rent that is too high for their income under the Rent Affordability Rules UK. |

| Reduce late or missed rent payments | Ensure rent is set at a level that renters can practically afford each month. |

| Encourage responsible budgeting | Helps renters plan their income and expenses more successfully. |

| Improve financial security | Supports both tenants and property owners by reducing investment risk. |

| Support better money management | Inspires stronger spending habits and financial planning through the Rent Affordability Rules UK. |

| Reduce the likelihood of debt problems | Prevents tenants from falling into arrears or borrowing to pay rent. |

| Create a safer tenancy experience | Makes renting more stable and less stressful for renters. |

| Help landlords select reliable tenants | Assist property owners and letting agents in choosing renters who are financially capable of paying rent regularly. |

| Avoid long-term financial difficulties | Avoid tenants from entering into contracts they may struggle to maintain later under the Rent Affordability Rules UK. |

| Promote stable rental agreements | Leads to longer, more secure rental agreements for both parties. |

Read More: Rent to Income Ratio Calculator UK – 7 Easy Ways to Save MoneyCommon Rent Affordability Rules Used in the UK

Different landlords and agencies may use different criteria, but several affordability checks are commonly applied.

Income Requirements

Most landlords require proof that your income is sufficient to cover rental payments comfortably.

Rent-to-Income Ratio

The proportion of your income spent on rent is carefully assessed.

Employment Verification

Applicants are often asked to provide proof of Job or a stable income source.

Credit History Check

A credit check helps landlords assess financial dependability and payment history.

Guarantor Requirement

If affordability requirements are not met, a Surety may be required to support the tenancy.

Click Here:Rent Affordability Rules UK – 8 How Much Rent Can You Afford

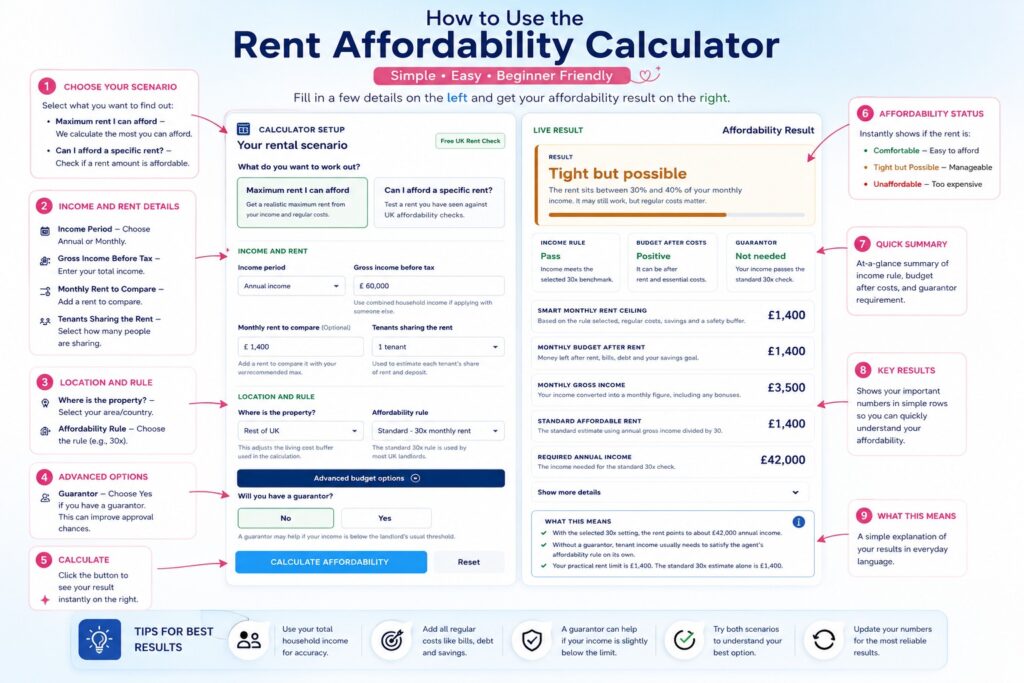

How to Use the Rent Affordability Calculator

Existing Financial Commitments

Landlords may consider:

- Personal loans

- Credit card balances

- Car finance agreements

- Student loans

Additional Income Sources

Some landlords may accept:

- Pension income

- Government benefits

- Freelance earnings

- Savings income

Read More: University Average CalculatorThe 30% Income Rule

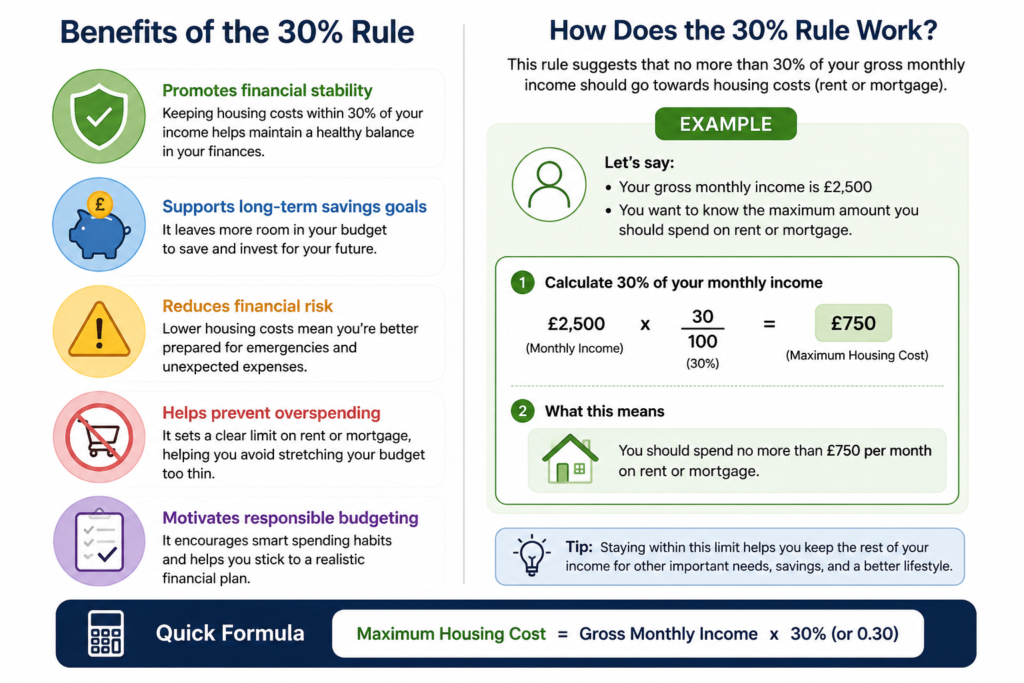

What Is the 30% Rule?

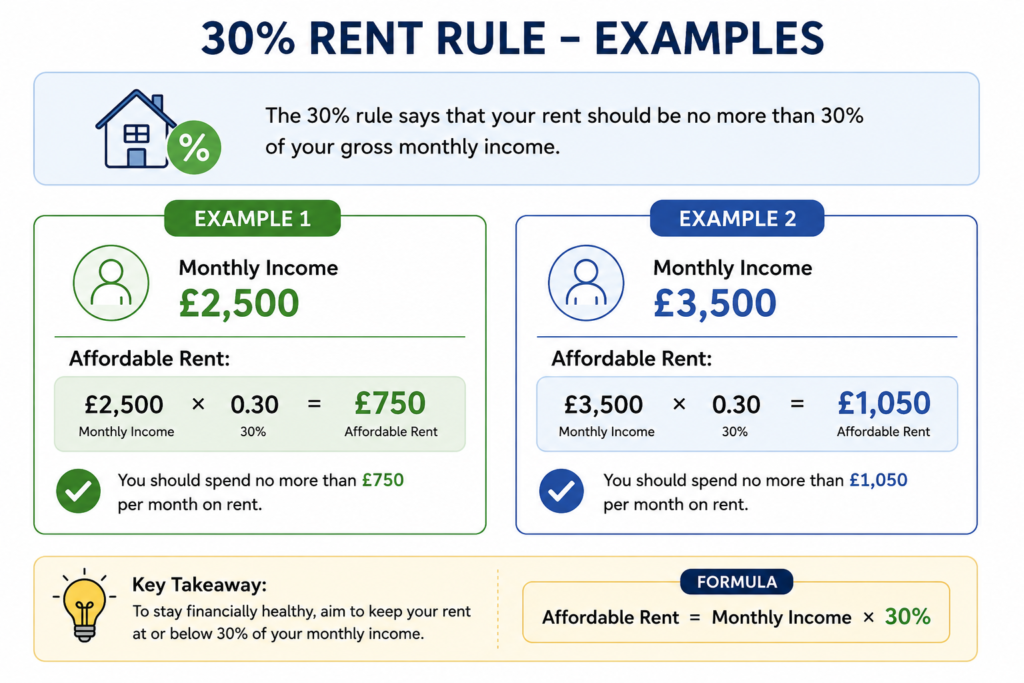

One of the most popular payability rules suggests spending no more than 30% of your income on rent and housing costs.

The goal is simple: ensure sufficient income remains available for daily expenses, savings, and emergencies.

| Monthly Income | 30% Rent Budget |

|---|---|

| £2,000 | £600 |

| £2,500 | £750 |

| £3,000 | £900 |

| £4,000 | £1,200 |

This rule is widely used because it provides a Simple way to determine reasonable rent levels.

Benefits of the 30% Rule

- Promotes financial stability

- Supports long-term savings goals

- Reduces financial risk

- Helps prevent overspending

- Motivates responsible budgeting

It is important to remember that this instruction is not a legal requirement. It simply serves as a practical Standard

The 50/30/20 Budget Rule

While the 30% rule focuses on housing costs, the 50/30/20 rule provides a broader budgeting framework.

| Budget Allocation | What It Includes |

|---|---|

| 50% for Needs | Rent, Utilities, Food, Transportation, Healthcare |

| 30% for Wants | Entertainment, Dining out, Hobbies, Shopping |

| 20% for Savings and Debt Repayment | Emergency funds, Investments, Savings accounts, Loan repayments |

While budgeting rules like the 30% and 50/30/20 methods help you set a personal ceiling, letting agents apply their own, often stricter, formulas when assessing your application and it’s worth knowing these before you view a property.

The 50/30/20 method helps renters maintain balance between spending and saving.

Letting Agent Income Requirements

Many letting agents use strict affordability formulas before approving an application.

Typical requirements include:

- Proof of employment

- Payslips

- Bank statements

- Income verification documents

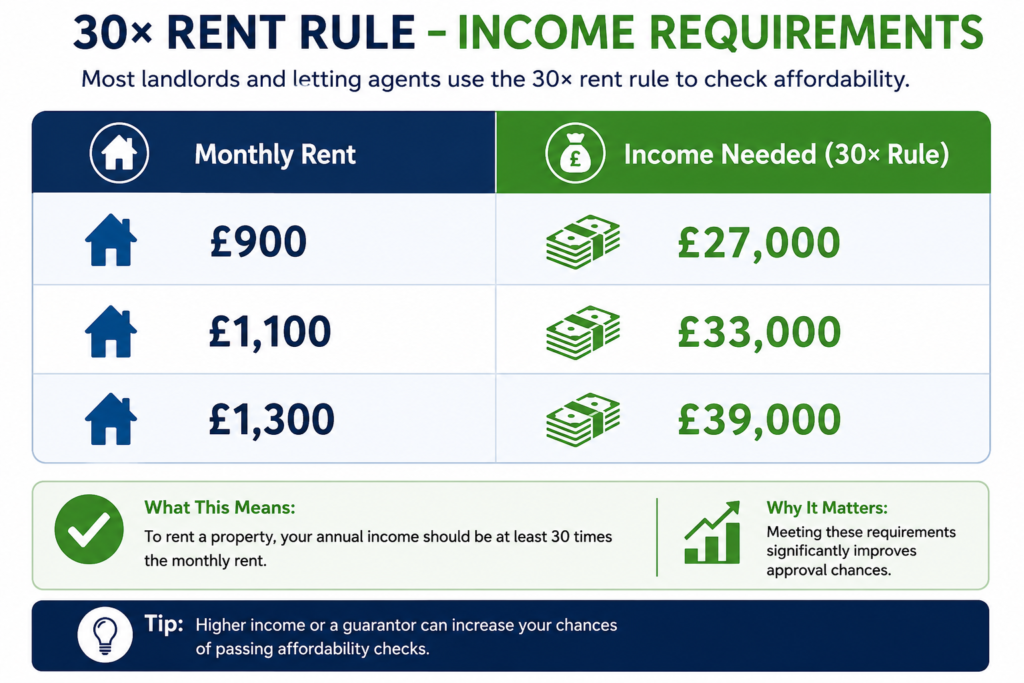

Some agencies require annual earnings equal to 30 to 36 times the monthly rent.

For example:

| Monthly Rent | Income Needed (30× Rule) |

|---|---|

| £900 | £27,000 |

| £1,100 | £33,000 |

| £1,300 | £39,000 |

Meeting these requirements significantly improves approval chances.

Affordability Checks for Self-Employed Renters and Benefit Claimants

| Income Type / Situation | How Affordability Is Usually Assessed |

|---|---|

| Fixed Monthly Payslip | Not every renter has a fixed monthly payslip, and landlords assess affordability differently depending on income type. |

| Self-Employed Applicants | Self-employed applicants are usually asked for 2–3 years of SA302 tax calculations or an accountant’s reference, plus recent business bank statements, since income can fluctuate year to year. |

| Universal Credit or Housing Benefit Claimants | Universal Credit or Housing Benefit claimants can still pass affordability checks, though some landlords ask for a guarantor if the housing element doesn’t fully cover the rent. Under the Equality Act 2010, landlords and agents cannot refuse an applicant purely for receiving benefits; a “No DSS” blanket policy has been found unlawful in UK courts. |

| Pension or Investment Income | Pension or investment income is typically averaged over the past 3–6 months of bank statements rather than judged on a single payslip. |

| Income Doesn’t Meet the Standard 30x Rule | If your income doesn’t fit the standard 30x rule, a guarantor earning roughly 36x the monthly rent annually (or holding sufficient savings) is the most common workaround letting agents accept. |

Affordability Checks by Landlords

Income Assessment

Landlords review whether your earnings can comfortably support rent payments.

Employment Verification

Stable employment often strengthens an application.

Document Review

Commonly requested documents include:

- Payslips

- Bank statements

- Employment contracts

Credit Checks

Credit reports help assess financial responsibility.

Financial Stability Review

Some landlords also evaluate overall financial health, including debts and regular monthly obligations.

How to Calculate Affordable Rent (Climax Section)

This is where affordability becomes practical.

Use the following formula:

Affordable Monthly Rent = Monthly Income × 30%

Example 1

Monthly Income = £2,500

Affordable Rent:

£2,500 × 0.30 = £750

Example 2

Monthly Income = £3,500

Affordable Rent:

£3,500 × 0.30 = £1,050

Example 3

Monthly Income = £4,500

Affordable Rent:

£4,500 × 0.30 = £1,350

Practical Scenario

| Scenario | Details |

|---|---|

| Name | Priya |

| Monthly Income (After Tax) | £2,800 a month after tax. |

| Recommended Rent Budget (30% Rule) | Using the 30% rule, her recommended rent budget is £840. |

| Rent of the Chosen Flat | She finds a flat at £950/month — over budget by £110. |

| Monthly Outgoings | Before ruling it out, she checks her outgoings: £150/month in mobile and streaming subscriptions, no existing debt, and £3,000 in savings. |

| Adjustment Made | By trimming £100/month in discretionary spending, she brings her effective affordability closer to £940, just under the asking rent. |

| Letting Agent Affordability Check | She still passes the letting agent’s 30x annual income check (£2,800 × 12 = £33,600, well above the £28,500 needed for £950 rent). |

| Key Takeaway | This shows why the 30% rule is a starting point, not a hard cutoff — it works alongside your actual spending and savings buffer. |

Quick Affordability Table

| Monthly Income | Recommended Rent |

| £2,000 | £600 |

| £2,500 | £750 |

| £3,000 | £900 |

| £3,500 | £1,050 |

| £4,000 | £1,200 |

| £5,000 | £1,500 |

This calculation provides a practical starting point before taking into account additional living expenses.

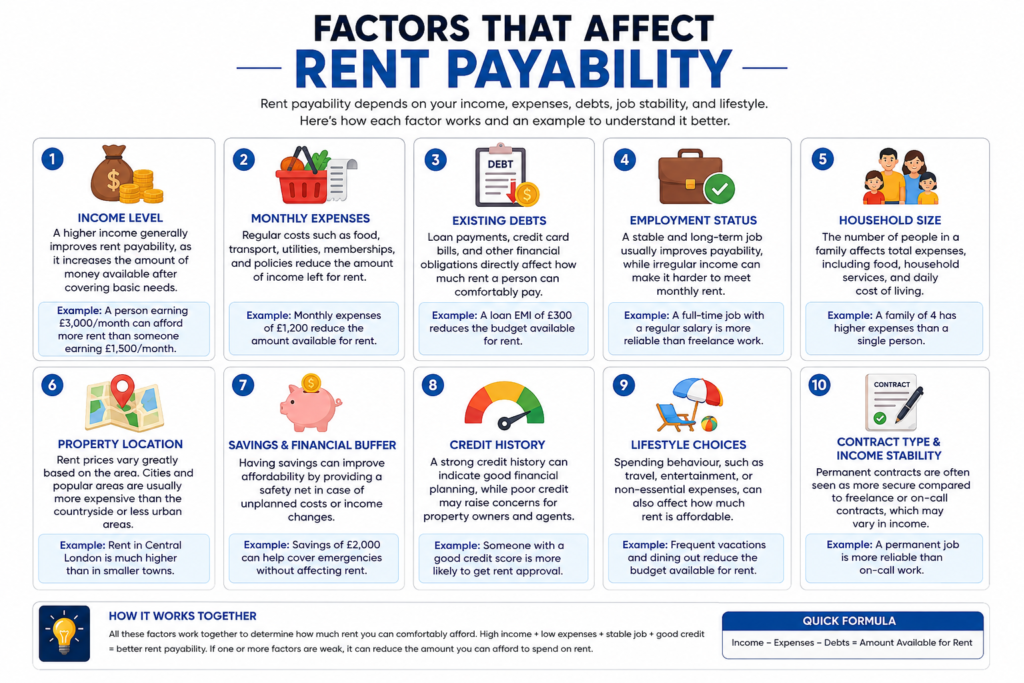

Factors That Affect Rent Affordability

Several personal and financial conditions can influence how much rent is really affordable for a tenant. These factors are usually reviewed during payability checks to ensure the rent matches the tenant’s real financial situation.

Income Level

A higher income generally improves rent payability, as it increases the amount of money available after covering basic needs.

Monthly Expenses

Regular costs such as food, transport, utilities, Memberships, and policies reduce the amount of income left for rent.

Existing Debts

Loan payments, Credit card payments, and other financial obligations directly affect how much rent a person can comfortably pay

Employment Status

A stable and long-term job usually improves payability, while Irregular income can make it harder to meet monthly rent

Household Size

The number of people in a family affects total expenses, including food, Household services, and the daily cost of living

Property Location

Rent prices vary greatly based on the area. Cities and Popular areas are usually more expensive than the countryside or less Urban areas

Savings and Financial Buffer

Having savings can improve affordability by providing a safety net in case of unplanned costs or income changes.

Credit History

A strong credit history can indicate good financial planning, while poor credit may express concerns for property owners and agents.

Lifestyle Choices

Spending behaviour, such as travel, entertainment, or non-essential expenses, can also affect how much rent is affordable.

Contract Type and Income Stability

Permanent contracts are often seen as more secure compared to freelance or On-call contracts, which may vary in income.

Debt and Loan Payments

Debt duties can greatly affect affordability calculations.

Examples include:

- Personal loans

- Mortgage repayments

- Student loans

- Car finance agreements

- Credit card repayments

Before choosing a rental property, ensure these commitments are factored into your budget.

Location and Cost of Living

Location can dramatically influence housing affordability.

In many UK cities:

- Rent levels differ significantly

- Utility costs vary

- Transportation expenses change

- Daily living costs Change

A property that seems affordable in one area may be financially difficult in another.

Tips to Improve Rent Affordability

Improving the ability to pay. Monthly payment often does not require major changes. With limited income growth and better decisions, you can significantly increase your ability to pay rent on time comfortably.

| Tip | Description |

|---|---|

| Increase income through additional work | Getting a half-time job or self-employed work can help increase the total monthly income. |

| Reduce unnecessary spending | Decreasing extra costs such as entertainment or unused plans can free up extra money for rent. |

| Follow a monthly budget | Creating and sticking to a clear budget helps record earnings and expenses more successfully and avoid spending too much. |

| Pay down existing debt | Reducing loan or payment card balances lowers monthly financial plan pressure and improves overall payability. |

| Choose a lower-cost property | Choosing a more reasonable home can make it easier to stay within a comfortable income-to-rent ratio. |

| Consider shared accommodation | Renting with others can greatly reduce individual rent and household bills. |

| Build an emergency savings fund | Having savings provides an emergency fund for emergency expenses and helps maintain rent payments during tough months. |

| Avoid lifestyle inflation | Keeping spending habits safe even when income increases helps maintain long-term financial ability. |

| Improve financial planning habits | Regularly checking expenses and changing your financial plan can help maintain better control over your financial situation. |

| Compare rental options carefully | Searching different areas and property types can help you find better value for money without focusing on basic needs. |

Common Mistakes When Calculating Affordable Rent

Excluding Council Tax,

Local taxes can greatly impact overall housing costs.

Underestimating Living Costs

Daily expenses are often higher than expected.

Ignoring Existing Debt

Debt repayments reduce available disposable income.

Choosing Rent Above Budget

Overstretching financially increases risk.

Not Saving for Emergencies

Unexpected costs can create financial pressure.

Using Gross Income Instead of Net Income

Take-home pay provides a more realistic affordability calculation.

Forgetting Future Expenses

Financial plans should consider future obligations.

Not Comparing Rental Options

Researching multiple properties often reveals better value.

Read more:Rent Affordability Calculator London – How Much Rent Can You Afford in LondonWhat is the 30% rent rule in the UK?

The 30% rule suggests spending no more than 30% of your monthly income on rent and housing costs.

How do landlords check rent affordability?

They typically review income, employment status, bank statements, and credit history.

Can I rent if I spend more than 30% of my income on rent?

Yes. However, doing so may increase financial pressure and reduce flexibility in your budget.

What income do I need to rent a property?

The required income depends on the monthly rent and the landlord’s affordability criteria.

Do affordability calculators include bills?

Some calculators include utility costs and council tax, while others focus solely on rent.

Are rent affordability calculators free?

Yes. Most online rent affordability calculators are free to use.

What is the 30% rent rule in the UK?

It’s a budgeting guideline suggesting no more than 30% of your net monthly income should go toward rent. It’s not a legal requirement or a rule every landlord uses — some apply the stricter 30x annual salary rule instead — but it’s a useful sense-check before you start viewing properties.

How do landlords check rent affordability?

Most use a referencing agency to verify your income (via payslips or an employer reference), run a credit check, and confirm your right to rent in the UK. Self-employed and benefit-receiving applicants may go through additional checks, such as tax calculations or a guarantor requirement.

Can I rent if I spend more than 30% of my income on rent?

Yes — many renters, especially in London and other high-cost cities, spend 40% or more. It’s not against any rule, but it leaves less room for savings and unexpected costs, so it’s worth budgeting carefully if you go above this threshold.

What income do I need to rent a property?

Most letting agents use the “annual income = 30x monthly rent” formula. For a £1,000/month property, that’s roughly £30,000/year. If your income falls short, a guarantor earning around 36x the rent can usually make up the difference.

Do affordability calculators include bills?

It varies. Most basic calculators only compare rent against income. More detailed ones — including some landlord referencing tools — also factor in council tax, utilities, and existing debt repayments for a fuller picture.

Are rent affordability calculators free?

Yes, and most letting agents and comparison sites (such as Rightmove and Zoopla) offer free versions as part of their listings.

Conclusion

Learning a reasonable rental property is about more than simply covering the monthly earnings.

By understanding UK rent ability-to-pay rules, applying the 30% guideline, and thinking about your full financial picture, you can choose a property that supports both your lifestyle and permanent financial balance.

Financial capacity is not a one-time calculation, either. Your income, costs, and life show change, and it’s worth revisiting your rent-to-income ratio every time your salary changes, before a repayable rental agreement, or whenever your monthly outgoings shift greatly. A property that was comfortably payable last year may feel more limited after a cost increase or new financial requirements.

The safest method is to treat the 30% rule as a starting point, not a final answer. Layer it with a real look at your bank statements, your existing loan, and a small savings buffer for urgent situations. Property owners and letting agents will run their own checks anyway, so doing this groundwork yourself means reduced surprises, reduced rejected applications, and a rental financial plan you can actually support— not just qualify for on paper.

Want me to also add a short closing call-to-action line (e.g., pointing readers to try a rent affordability calculator or check their numbers before applying)?